How the payments industry is being disrupted

The danger from disruptions for the payments industry today, the future scenario of disruption, the responses of payment firms, and the “blinders” in their responses

1. Introduction

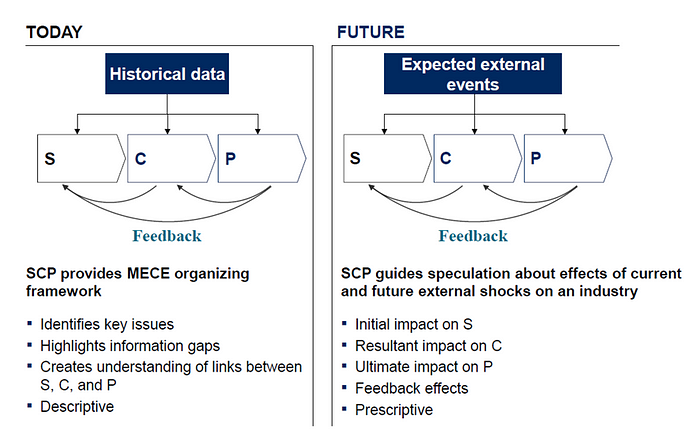

In this article I will analyse the payments industry — or ecosystem. I will explain the danger the pure pipeline incumbents face from existing disruptions¹. To explain the danger payment companies face from disruptions and the scenario that is likely to materialize in the near future, I will apply the framework of the Ecosystem assessment in which the boundaries of the industry have disappeared². The framework uses the dimensions Structure, Conduct, and Performance (SCP) to analyse the past and forecast the future (see Fig. 1).

First, I will use the SCP as a MECE organising framework to assess the threat from digital disruption in the payments industry today. Second, I will apply the SCP framework to assess the effects and scenarios of current external shocks on the industry in the future.

2. Danger from disruptions for the payments industry today

2.1 Digital disruptions along the payments value chain

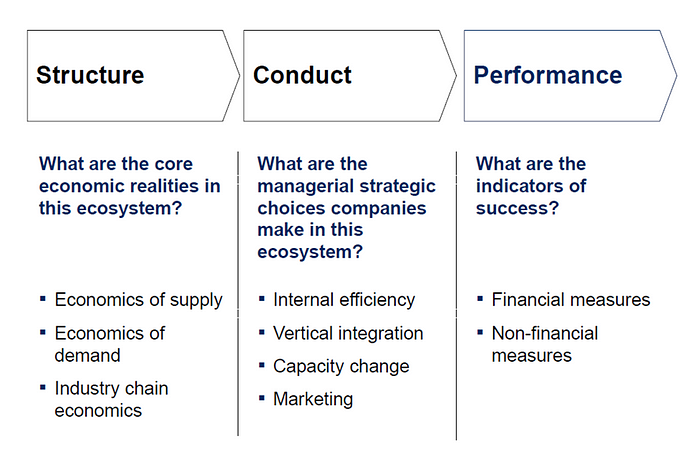

To explain the current threat of disruptive innovations for the payments industry, I analysed the core economic realities in the payments ecosystem (Structure), the managerial strategic choices (Conduct), and the indicators of success (Performance) along the payments value chain (see Fig. 2)³. In addition, I identified the next sources of value attractive in terms of market potential along the value chain⁴.

To identify disruptive innovation, I am following the broader than the classical definition of Christensen⁵ from Ansari⁶ who defines disruption as “anything that attacks the basis of [the company’s] competitive advantage”. Therefore, disruptive innovation is threatening the whole payments value chain — from the customer lifecycle with acquisition, management, and servicing to remote and proximity payments itself. Disruption takes place first around the customer lifecycle, second the types of payments from a customer perspective and third from the merchant perspective as well as fourth value-added services (VAS) around the purchase cycle.

2.1.1 Disruptive innovations around the customer lifecycle

Digital disruption around the customer lifecycle, specifically in the account acquisition management, customer management, and servicing phase are research and acquisition, application and processing, fulfilment and activation, and ongoing usage and retention.

In the first research and customer acquisition phase, banks are investing heavily in acquisition to drive customers to their websites, primarily through disruptions in targeting and selection, digital marketing and channel capabilities as well as information and support tools.

In the second application and processing phase, digital disruption — specifically in the form of new delivery channels — can be identified around the lifecycle activities⁷. Disruptive innovation takes place in application funnel management, channel application capabilities, security, and application support as well as the enhancement of data and capabilities.

In the third fulfilment and activation phase, the disruptive innovation contains digital communication and digital activation. The fourth ongoing usage and retention phase, disruption takes the form of digital communication, account access, channel functionality, loyalty, and digital engagement. The fifths underlying phase, the traditional servicing, is disrupted by new digital servicing solutions.

2.1.2 Disruptive innovations around payments

The disruptive innovation battleground in digital payments is open to changes with new players and technologies. Digital innovation around payments takes place within the dimensions P2P — with Domestic and International — and P2B — with Proximity (In-store/in-app) and Remote (Online). Disruptive players are card companies, ACH providers and other e-money, cryptocurrencies, etc. ecosystem stakeholders. Specifically, P2B in-app and online payments are converging to mobile.

The disruptive innovation battleground in acquiring (P2B) is more crowded with non-bank entrants serving small, online merchants⁸. These non-bank competitors disrupt primarily through radically different business model solutions in in-app and online payments⁹. The online world offers, both for consumer and merchants, a greater selection in payment type and platform choice along the phases commerce interface, underlying integration, checkout, processing and settlement, and clearing.

Apart from the payment, both merchants and customers look for value-added services around full the purchase cycle. While issuers are best positioned to deliver consumer VAS for consumers, acquirers and PSPs can work independently with merchants to deliver value-added services.

3. Future scenario of disruption in the payment ecosystem

To predict the future scenario of disruption in the payment ecosystem, I analyse the impact of expected external events by using the SCP framework. The Framework contains external disruptive events that initially impact the Structure, then the resulting Structure impacts the Concept, which ultimately impacts the performance, and feedback to the Structure.

3.1 Primary external disruptive events

Primary external disruptive events in banking and payments are digital adoption, increased fragmentation, and standardization. The impact on the Structure is that the payments market is shifting rapidly with digitalisation and competition.

First, digital adoption is driven by growing Internet, mobile and tablet penetration over the past years. The development has shown that mobile devices are an integral part of daily life. In addition, with the increasing mobile penetration and new solutions e-commerce will continue becoming increasingly mobile.

Second, fragmentation is driven by digitization in the form of new technology which changes the dynamics in the payments industry¹⁰; in contrast to that the banking industry is used to enjoy strong barriers to entry. Consequently, banks — and transaction banks despite their high profitability and scale advantage — are increasingly concerned about disruptive players coming into the market¹¹. Third, standardisation is driven by regulation which is putting pressure on the digital payments space.

3.2 Secondary external disruptive events

Secondary external events are consumer preferences which are changing in favour of convenience, value-added services, and an omni-channel experience. The impact on the Structure is that consumers prefer a seamless and end-to-end experience across digital devices.

First, driven by convenience and other practical benefits, mobile banking is the new way to interact. Furthermore, when it comes to payments, convenience and security are key for issuing. Second, value-added interaction is driven by a multi-faceted digital interaction with functional and value-added solutions. Third, convergence brings in new ways to deliver convenience and security.

3.3 Tertiary external disruptive events

Tertiary external events are the radical digital innovations per se¹². Therefore, banks need to leverage emerging technologies, innovations, and partnerships to stay ahead of the curve. The impact of digital innovations on Structure changes technologies, the disruptive innovation, and strategic partnerships.

First, emerging digital solutions enable new ways of paying by mobile both in-store and online payments. Three main technologies are currently vying for a role in powering mobile merchant interaction — NFC, QR codes, and Bluetooth. In addition, a rapid development is taking place in identification and authentication which is driven by non-traditional players.

Second, regarding innovation, banks are actively promotion innovation throughout their organisation. Third, regarding partnerships, banks will need partners to extend their capabilities and accelerate the time to market while keeping costs to minimum.

4. Responses of payment firms to disruptions

Issuers take different digital strategic responses to cope with the threat — from pure digital focus to minimum.

4.1 Responses around the customer lifecycle

To respond to disruptive innovations around the customer lifecycle, banks and payment companies respond with best practices in account acquisition and customer management.

4.1.1 Research and acquisition

In the research and acquisition phase, banks respond with heavy investment in acquisition to drive customer to their websites. In the dimension targeting and selection, for example, Tesco uses location-based offerings like GeoMapping to increase the relevance of their credit card programs. In the dimension digital marketing and channel capabilities, issuer need to have a strong presence across different digital channels. In addition, banks are aware that customer acquisition is not the focus of social media channels. As information and support tools, many banks are using a pre-application check, an Approval Indicator, as a quick and easy process to determine the likelihood of acceptance.

4.1.2 Application and processing

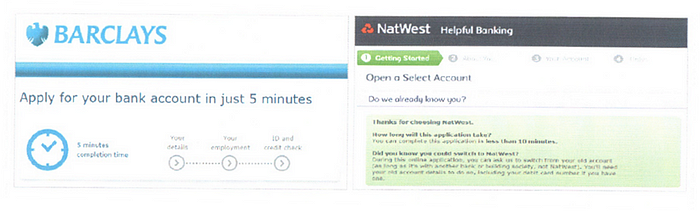

For application and processing, in the context of the application funnel management some banks like Barclays and NatWest provide a clear, efficient application form, keep the customer engaged through a clear signpost indicating application process (see Fig. 3). For channel application capability, the application through mobile apps has not taken off, yet. For security and application support, Barclays makes it easy for prospects to apply for a business bank account. To enhance data capabilities, issuer use alternative data for “thin file” credit decisions.

4.1.3 Fulfilment and activation

To respond to the disruptive challenges around fulfilment and activation, digital communication and digital activation is key for banks. For digital communication, banks increase the number of fulfilment and activation channels to improve customer penetration. For digital activation, banks provide PINs digitally to encourage activation. Beyond that, best in class banks allow card activation via mobile application. Banks use early purchase-specific incentives more aggressively to drive activation.

4.1.4 Ongoing usage and retention

To respond to the disruption in usage and retention, banks are offering digital communication, account access and security, channel functionality, loyalty and rewards, and digital engagement.

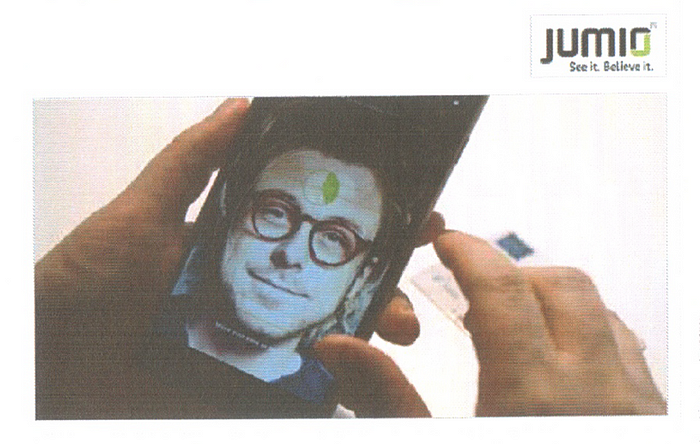

For digital communication, iGaranti and Akbank Direkt mobile banking apps offer sophisticated notification centres. To sum up, best practices is the use of multiple channels by an issuer to announce new mobile application and features. For account access and security, US Bank is pioneering voice biometrics, whereas a feature from Jumio compares a person’s face to their ID (see Fig. 4). For channel functionality, Iceland’s Meniga is giving customer more insight into their finances. In general, real-time receipts have a strong value proposition for all stakeholders involved. For loyalty and rewards, high customer expectations mean that banks need to innovate to stay competitive. For digital engagement, K-SME Business Plus creates a shared community of cardholders that provide rewards and business support. To sum up, in the UK marketing strategy in social media aimed at creating customer confidence with education at its core.

4.1.5 Servicing

To respond to the disruptions in traditional servicing, banks offer digital servicing. Customer service touch points and communications are relevant to the cardholder. Video conferencing as a service is an example of technology transforming banks.

4.2 Responses around payments

4.2.1 Responses around payments from customer perspective

To respond to the disruptions in the innovation battleground in digital payments, players converge from P2B in-app and online payments to mobile¹³. For example, Apple Pay offers one-touch payments at POS and in-app payments with a focus on security and safety rather than loyalty programs.

4.2.2 Responses around payments from merchant perspective

To respond to disruptions on the acquiring side, merchants offer solutions for primarily in-app and online payments. For example, MCX is a mobile commerce network which is built by merchants for merchants to streamline the customer shopping experience at POS.

4.3 Reponses around value-added services

To respond to the disruptive challenges in VAS, both merchants and payment companies try to offer value service around the full purchase cycle. For instance, merchant value-added services for pre-purchase are Shop Small or Quare Analytics. The first offers a search and discovery application, whereas the second provide marketing analytics. For merchant value-added services in purchase, VISA Security, for instance, offers security. For merchant value-added services in post-purchase, Shopify provides logistic and inventory. For other selected merchant VAS solutions, Advance America, for example, offers payday loan.

5. “Blinders” in the payment companies’ responses

To identify the “blinders” and information gaps in the payment companies’ responses, I used the SCP framework. I identified that “blinders” are often not the digital initiatives; they are rather the lack in digital transformation and operating model. In general, banks and payments companies miss out on the opportunity of disruptive innovation strategy to completely rethink their whole operating model — from organisation through segments to technology and infrastructure.

As outlined in the previous chapter, most banks respond to some degree and transform pieces of their business. But they lack the transformation of the entire value chain and their business model. Change is only limited to new sales channel, service apps, or automating some processes.

First, they miss out on the operating model design to mirror the execution choices to help successfully deliver on the digital strategy. They often do not align them with the organisation such as product, segment, channel, sales, marketing, and IT. The banks’ operating model is not flexible enough to realise their digital strategy. They are not capable to develop plans for how they will create and capture feasibly in terms of the bank’s resources and capabilities the identified next sources of value¹⁴. Furthermore, they do not align with the segment of tech savvy, traditional, and unbanked customers and of large and small merchants. The key to success is to understand how banks can better service different segments via digital.

Second, they fail the technical design to mirror the disruptive execution choices to help them successfully deliver on the digital strategy. For instance, the front end is often not prepared for exponential growth in traffic and data. The middleware lacks new functionalities and real time information processing via Kernels. In addition, the backend is often not a lean core banking system with by design-enabled digital banking and CRM. The key is to set the bank up to meet with the major technology challenges in delivering on their digital banking strategy.

6. Conclusion

To sum up, challenge of disruptive innovation has not only implications for the digital initiatives itself, but also for the technology that support them, the people and culture who need to implement them, and the processes that govern them¹⁵. Banks often miss out on the challenges each stage of the transformation presents. Firstly, CEOs fail in setting digital transformation at the core of the banks and payments companies’ agenda. Secondly during the launch and acceleration phase, banks often fail to keep the launched digital change initiatives afloat and spawn more. Thirdly, in the 18-month time range, they fail to scale the up-and-running digital initiatives across the organisation. Banks would be better off if they apply the 3 Box Model from Ansari¹⁶ to holistically balance the past-present-future of their digital transformation. This implies for bank CEOs to selectively forget the past, continue to manage the present, and in addition create the future.

7. References

[1] Van Alstyne, M.W., Parker, G.G. and Choudary, S.P. (2016) Pipelines, Platforms, and the New Rules of Strategy, Harvard Business Review, April 2016 issue, p. 57f

[2] Goodman, A. (2021) The Music Business in Era of Disruption, Disruptive Technology & Innovation Lecture Unit 3, 3/8; Ansari, S. (2021) Disruptive Innovation, Disruptive Technology & Innovation Lecture Unit 1, 1/8; Munir, K.A. (2021) Good Strategy v Bad Strategy, Judge Business School University of Cambridge, p. 2ff

[3] Goodman, A. (2021) The Music Business in Era of Disruption, Disruptive Technology & Innovation Lecture Unit 3, 3/8

[4] Ansari, S. (2021) Disruptive Innovation, Disruptive Technology & Innovation Lecture Unit 1, 1/8; Munir, K.A. (2021) Disruptive Technology & Innovation Lecture Unit 4, 4/8

[5] Christensen, C.M., Raynor, M.E. and McDonald, R. (2015) What Is Disruptive Innovation? Harvard Business Review, December 2015 issue, p. 46f

[6] Ansari, S. (2021) Disruptive Innovation, Disruptive Technology & Innovation Lecture Unit 1, 1/8; King, A.A. and Baatartogtokh, B. (2015) How Useful Is the Theory of Disruptive Innovation? MIT Sloan Management Review, Vol. 57, №1, p. 80

[7] Ansari, S. (2021) Disruptive Innovation, Disruptive Technology & Innovation Lecture Unit 1, 1/8

[8] McKinsey (2020) The 2020 McKinsey Global Payments Report, McKinsey, October 2020, p. 13ff

[9] Ansari, S. (2021) Disruptive Innovation, Disruptive Technology & Innovation Lecture Unit 1, 1/8

[10] Ansari, S. (2021) Disruptive Innovation, Disruptive Technology & Innovation Lecture Unit 1, 1/8

[11] Ansari, S. (2021) Disruptive Innovation, Disruptive Technology & Innovation Lecture Unit 1, 1/8; Alevizakos, A., Yang, F., Down, R. and Vijayarajah, K. (2018) Transaction banking and securities services: Fintech is a friend not a foe, HSBC Global Research, 6th April 2018, p. 1ff; Graseck, B. and O’Kelly, R. (2021) Striving to Sustain Returns, Morgan Stanley and Oliver Wyman, p. 6f

[12] Benner, M.J. (2010) Securities Analysts and Incumbent Response to Radical Technological Change: Evidence from Digital Photography and Internet Telephony, Organization Science, Vol. 21, №1, January–February 2010, p. 1ff

[13] Tracxn (2020) FinTech — Top Business Models Report, December 23, 2020, p. 18

[14] Ansari, S. (2021) Disruptive Innovation, Disruptive Technology & Innovation Lecture Unit 1, 1/8

[15] Walker, B. and Soule, S.A. (2017) Changing Company Culture Requires a Movement, Not a Mandate, Harvard Business Review, June 20, 2017, p. 1ff; Sull, D., Sull, C., and Chamberlain, A. (2019) Measuring Culture in Leading Companies, MIT Sloan Management Review, June 2019, p. 1ff

[16] Ansari, S. (2021) Disruptive Innovation, Disruptive Technology & Innovation Lecture Unit 1, 1/8

Thanks for reading! Liked the author?

If you’re keen to read more of my Leadership Series writing, you’ll find all articles of this weekly newsletter here.

Go Beyond

Tech for sustainable growth

Tech for sustainable growth Here comes a gentle introduction to tech for sustainable growth by…

ESG rollback and its global impact in ESG Leadership by Victoria Riess

ESG rollback and its global impact in ESG Leadership by Victoria Riess “The rollback of…

Technology and recruitment

Technology and recruitment What is the role of technology in recruitment? RW05 — Technology and recruitment Well,…